Tesla Robotics, AI and Outlook post Q1

Tesla Robotics, AI and Outlook post Q1

Thoughts from a biological neural net on digital neural nets

Tesla Robotics

The breakthrough in LLMs could well be the final piece in the puzzle that was missing to develop a useful humanoid robot. Previously, robots were already well able to process their surroundings with convolutional neural networks. Similarly, with reinforcement learning, robots could be trained to master a narrow set of tasks extremely well, such as defeating the Go world champion or playing a game of video golf. However, there was no math to really understand what a human was saying and then translate that into a useful response. Obviously with LLMs this is no longer the case. So all the components could well be in place to pre-train humanoid robots to handle a wide variety of tasks in either factory or home environments, and with an LLM the robot can be instructed by humans on what to do. While the robot is still much slower than a human, it can work 24 hours per day, needing only some breaks to recharge the battery.

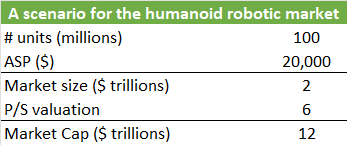

Now if this scenario plays out successfully over the coming decade, we should be looking at a massive market. Taking a scenario where the humanoid robotic market would be similar in units to the annual passenger vehicles market, say around 100 million units or so, this would translate into $12 trillion market cap for the companies involved:

Naturally if robots can carry out a wide variety of tasks, these estimates will be way too small. Elon Musk estimates we should be looking at 2 to 3 robots for every human on the planet and assuming a lifespan of 6 years for the average robot, this would result in an annual market of 3 billion units.

It’s also possible that these robots can be rented out with a subscription model as we have in SaaS software, which would again result in an even much larger market size. Anyways, whichever numbers you prefer to put in into the model, it’s clear that if this technology can be successfully developed, the market is likely going to be enormous and early investors will do extremely well.

This is Musk on Tesla’s recent call discussing the company’s Optimus humanoid robot:

“We are able to do simple factory tasks or at least, factory tasks in the lab. We do think we will have Optimus in limited production in the factory and doing useful tasks before the end of this year. And then I think we may be able to sell it externally by the end of next year. These are just guesses. As I've said before, I think Optimus will be more valuable than everything else combined. Because if you've got a sentient humanoid robot that is able to navigate reality and do tasks at request, there is no meaningful limit to the size of the economy. And I think Tesla is best positioned of any humanoid robot maker to be able to reach volume production with efficient inference on the robot itself. This, perhaps, is a point that is worth emphasizing. Tesla's AI inference efficiency is vastly better than any other company, there's no company even close. We've had to do that because we were constrained by the inference hardware in the car, we don't have a choice.”

I’ve linked a good video of Optimus’ latest capabilities and in my opinion, the latest version is doing some very impressive things. When Elon showcased the first version in ‘22 at their AI day, frankly, I thought it was a joke. The thing couldn’t even walk and they had only managed to train it to move its arms. Naturally they had only been working on it for a few months at that stage but it looked like they were years behind other companies in the field. But then in a timespan of just a little more than one year, it’s clear that the company has made tremendous progress and it’s by far the best and most naturally moving humanoid robot I’ve seen:

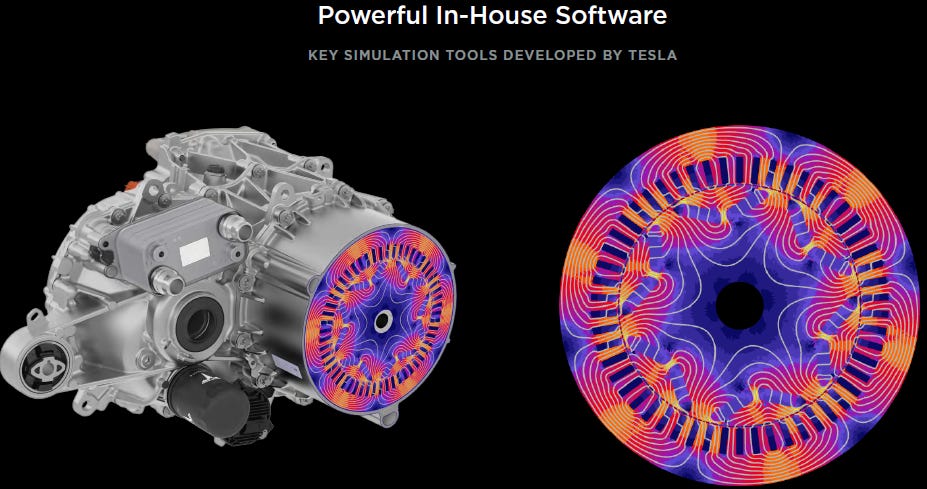

This rapid progress can only be explained by Tesla’s hardcore engineering culture, with the company having by far some of the most talented engineers in the world. The company designs most of their used vehicle components in-house, from large single-piece vehicle structures to small parts optimized for a single task. With the model 3, around half of controllers were designed in-house and Tesla reckons that with the next-gen vehicle they can bring this number up to 100%. The company is extremely vertically integrated and has a hardcore engineering ethos throughout, something which Musk has installed in each of his companies. As just one other example, Tesla has even written its own physics simulation software, something which competitors typically purchase from Ansys or Altair:

So the company is extremely well positioned to compete in the humanoid robotics market. It has not only massive scale in manufacturing and R&D, but also a hardcore engineering workforce that can design the robot’s components, software and semiconductors. As a result, it will come as no surprise that all of Optimus’ components are designed in-house: the actuators, sensors, electric motor, gearbox, power electronics and battery pack. The robot will carry a battery pack with sufficient power for a full day of work.

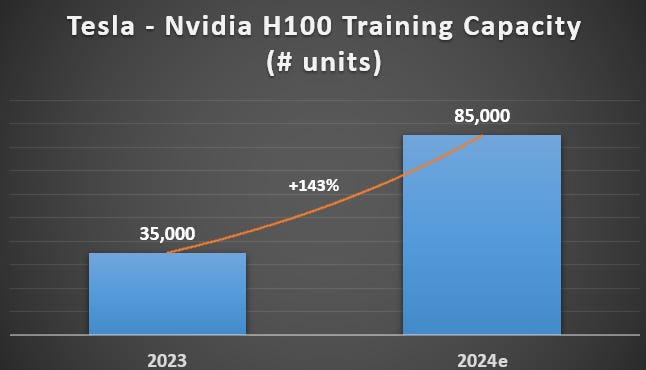

In addition, the company is extremely well positioned in AI. Not only does the company have one of the largest training clusters in the world, something which other robotic makers will struggle with..

But the company can also leverage their vehicles’ full self driving AI system to implement perception for Optimus. So a lot of AI training for the vehicles can be used directly in Optimus. Lastly, Tesla has good skills in semi design, the company has been designing its own FSD chip for on-vehicle inference for example:

Overall, Tesla should have all the ingredients in place to succeed in this market, from hardcore know-how and scale to design Optimus’ hardware components, to the expertise and scale to train the advanced AI software powering the robot. Finally, the company has multiple large manufacturing sites where the robot can be trained in real environments and on a large variety of tasks to optimize its neural nets.

Tesla AI

This brings us to the AI to self-drive the Tesla vehicles. While I’m still more sceptical on Tesla’s full self driving approach, as it seems like an incredibly hard problem to solve by purely relying on cameras as the inputs for the AI model, the company has made without any doubt a lot of progress by making the shift to end-to-end neural nets in the latest FSD 12. End-to-end neural nets means basically that all the decision making happens over neural nets, from processing the camera inputs to the end decision making what the vehicle will do next. Previously, there would lots of lines of C++ code to assist the model. This is Musk discussing these latest changes:

“Regarding FSD V12, which is the pure AI-based self-driving, if you haven't experienced this, I strongly urge you to try it out. It's profound and the rate of improvement is rapid. And we've now turned that on for all cars from Hardware 3 on in North America. So it's been pushed out to around 1.8 million vehicles and we're seeing about half of people use it so far, and that percentage is increasing with each passing week. So we now have over 300 billion miles that have been driven with FSD V12. It's become very clear that the vision-based approach with end-to-end neural networks is the right solution for scalable autonomy and it's really how humans drive. Our entire road network is designed for biological neural nets and eyes. So naturally, cameras and digital neural nets are the solution to our current road system. To make it more accessible, we've reduced the subscription price to $99 a month, so it's easy to try out.”

The goal is to launch a robotaxi fleet, where you can order a ride just like you do on Uber. Tesla has an advantage here as it can leverage its current fleet of millions of cars where owners can decide to rent out their vehicles if they wish to make an extra buck. This is Elon discussing the company’s future move into ride sharing:

“That will be how cars work, you just summon the car using your phone, you get in, it takes you to a destination and you get out. So you can think of Tesla like some combination of Airbnb and Uber. Meaning that there will be some number of cars that Tesla owns itself and operates in the fleet and there will be a bunch of cars where they're owned by the end user. That end user can add or subtract their car to the fleet whenever they want, and they can decide if they want to only let the car be used by friends and family, only by 5-star users, or by anyone. At any time, they could have the car come back to them and be exclusively theirs, like an Airbnb, you could rent out your guestroom or not any time you want.

We have 9 million cars, going to eventually tens of millions of cars worldwide. With a constant feedback loop, every time something goes wrong, that gets added to the training data and you get this training flywheel happening in the same way that Google Search has the sort of flywheel. It's very difficult to compete with Google because people are constantly doing searches and clicking and Google is getting that feedback loop.”

This is the company’s head of AI going deeper on how they’re constantly retraining and evaluating the models:

“In any given week, we train hundreds of neural networks that can produce different trajectories for how to drive the car, and we replay them through the millions of clips that we have already collected from our users and our own QA (quality assurance) network. Those are critical events, like someone jumping out in front, that we have gathered in the database over many years. And then we have simulation systems, where we try to recreate and test this in close to fashion. Once this is validated, we give it to our QA networks. We have hundreds of them in different cities, San Francisco, Los Angeles, Austin, New York, a lot of different locations. They are also driving and collecting real-world miles, and we have an estimate of how they are a net improvement compared to the previous week builds. Once we have confidence that the build is a net improvement, then we start shipping to early users, like 2,000 employees initially. They will give feedback if it's an improvement or if they're noting some new issues that we did not capture in our own QA process. And only after all of this is validated, then we go to external customers. We have live dashboards of monitoring every critical event that's happening in the fleet, sorted by the criticality of it. So we are having a constant pulse on the build quality and the safety improvement along the way. Any failures, we'll get the data back, add it to the training and that improves the model in the next cycle.”

Tesla has been training their models on how the best drivers in their fleet steer the vehicle. This definitely makes a lot of sense as the model can learn from the best human drivers on the planet. While obviously adding the above feedback loop for critical events gives the model access to a massive scale of data to deal with fringe events. Data quality and quantity are the key competitive advantages in AI training so this could actually work. However, from what I’ve seen so far, FSD is not near robotaxi level (yet) as still regular interventions are needed. It is a very good eyes-on system that can manage to drive you fully to your destination, however, you really need to monitor the system continuously as it might make the occasional stupid mistake.

Tesla’s Outlook post Q1

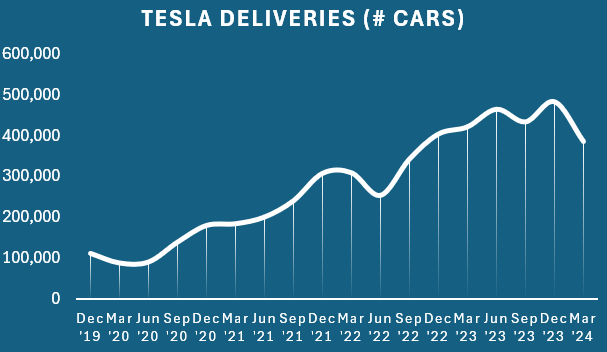

While the above longer term opportunities should be attractive, in the meanwhile, the market environment for electric vehicles (EVs) remains highly competitive. In addition, the industry has now entered a cyclical correction:

This is the company’s CFO discussing the cycle and margins, the latter which seem to be holding up well:

“We did see a decline in revenues quarter-over-quarter and these were primarily because of seasonality and the uncertain macroeconomic environment. Auto margins declined from 18.9% to 18.5% excluding the impact of Cybertruck. The impact of pricing actions was largely offset by reductions in per unit costs and the recognition of revenue from the Autopark feature for certain vehicles in the U.S. that previously did not have that functionality. Additionally, while we did experience higher cost due to the ramp of Model 3 in Fremont and disruptions in Berlin, these costs were largely offset by cost reduction initiatives.

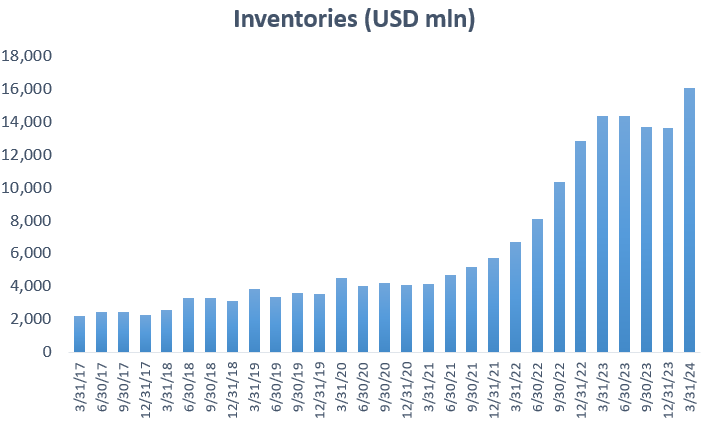

We had negative free cash flow of $2.5 billion in the first quarter. The primary driver of this was an increase in inventory from a mismatch between builds and deliveries as discussed before, and our elevated spend on CapEx across various initiatives, including AI compute. We expect the inventory build to reverse in the second quarter and free cash flow to return to positive again. As we prepare the company for the next phase of growth, we had to make the hard but necessary decision to reduce our headcount by over 10%. The savings generated are expected to be well in excess of $1 billion on an annual run rate basis.”

Tesla had their worst ever quarter on a FCF basis, however, if they spent one billion dollars on Nvidia GPUs this should be a good investment. The company still has $27 billion in cash on the balance sheet, so the financial position remains extremely healthy and next quarter should again be cash generative.

The largest driver was indeed the $2.4 billion rise in inventory levels:

Besides the EV market getting back into a positive upwards cycle, what should be an accelerator to sales growth for Tesla in the coming years is the launch of new models, including more affordable ones. This is Musk on Tesla’s model roadmap:

“We've updated our future vehicle lineup to accelerate the launch of new models ahead. I previously mentioned start of production in the second half of 2025. These new vehicles, including more affordable models, will use aspects of the next-generation platform as well as aspects of our current platforms, and we'll be able to produce on the same manufacturing lines as our current lineup. So it's not contingent upon any new factory or massive new production line. It will be made on our current production lines much more efficiently. And we think this should allow us to get to over 3 million vehicles of capacity when realized to the full extent.”

So if the company can then ship around 750,000 units per quarter from its existing installed lines, this would be a 50% increase from the peak delivery numbers Tesla generated during the previous quarter. Needless to say this will be extremely cash generative.

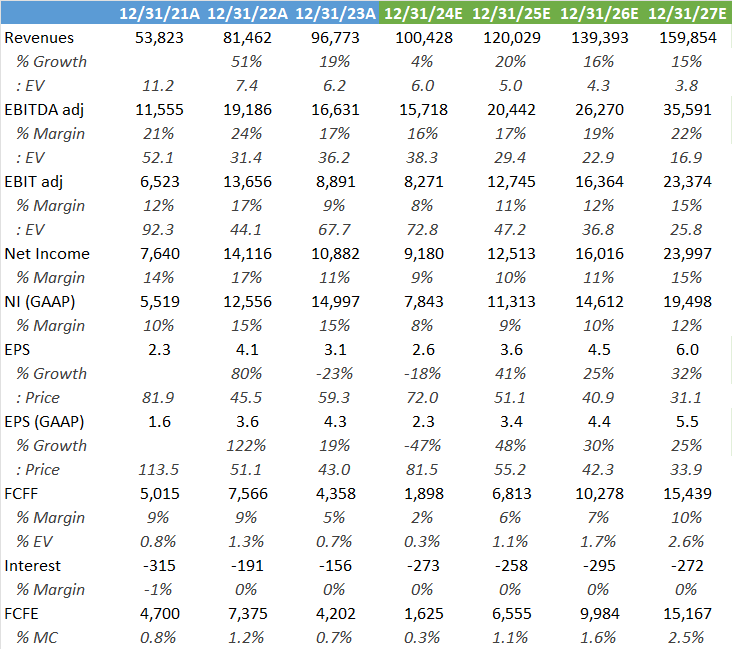

That said, if you’re not a believer in a significant opportunity coming from AI, frankly, it won’t make sense to hold these shares. This stock is already on 67x next-twelve-months’ EPS and even the best car companies in the world have a history of only trading around 10x at best e.g. Toyota. So while EVs remain a compelling growth story, the market is already pricing in Tesla’s EPS to go up almost seven fold, and much more once you start taking into account the cost of capital.

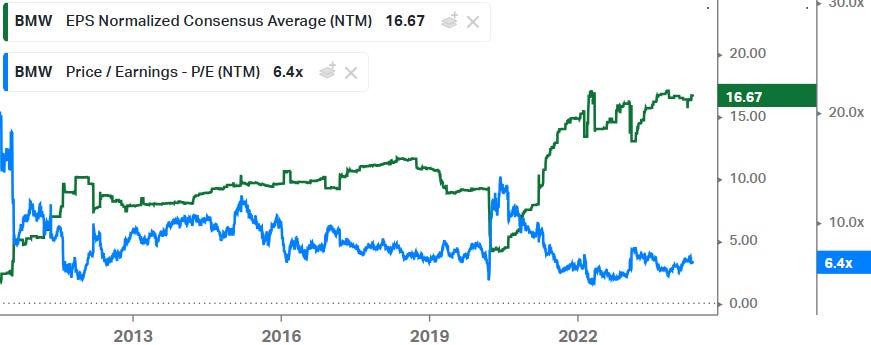

An example below of how the best car companies in the world tend to trade at low multiples, in this case BMW. Hardcore fans of Tesla will probably make the argument that the company will trade on an Apple or Ferrari multiple at maturity, but at this stage I’m still seeing the EV market as being too competitive for that to be the case. I can only see this scenario playing out if the company has substantial differentiation on the software side, e.g. the AI driving the car.

Given that the automotive market remains a highly competitive industry, and especially in EVs where we have seen a plethora of new entrants, I don’t see Tesla’s valuation offering attractive risk-reward. However, if you think that there is significant probability that the company can capture a strong share of the humanoid robotics or robotaxi markets, suddenly the valuation becomes a lot more attractive.

If you enjoy research like this, hit the like and restack buttons, and subscribe if you haven’t done so yet. Also, please share a link to this post on social media or with others who might be interested, it will help the newsletter to grow, which is a good incentive to publish more.

I’m also regularly discussing tech stocks on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. Before making any investment, it is recommended to do your own due diligence.