Inside the AdTech Industry: The Trade Desk's Problems & Outlook

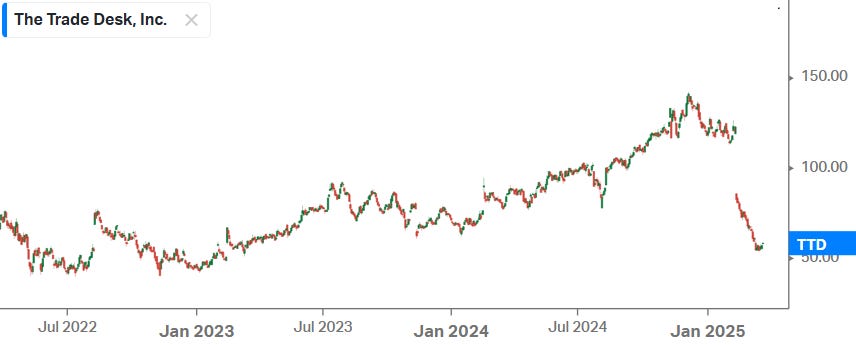

Falling knife or buying opportunity?

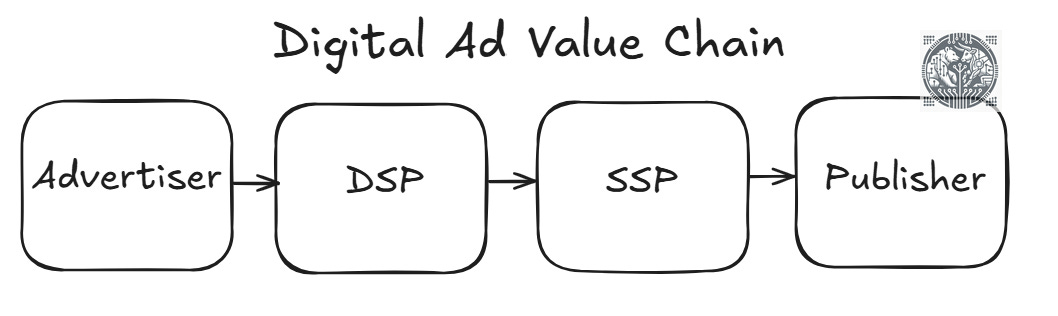

An Introduction to the Digital Ads Value Chain & The Trade Desk

Traditionally, publishers such as the Wall Street Journal sold advertising space in their media by closing large deals with ad agencies. The agency was the key player in the middle, connecting publishers to brands. This intermediary had the know-how to run advertising campaigns and as they purchased ad inventories in bulk, they also typically could offer brands a better deal.

In the internet era, this value chain started to fragment considerably and a wide variety of new players emerged. First, there are the ad networks, which dominate large swaths of the online advertising market. This is why the two dominant ad networks, Google and Meta, are amongst the largest companies in the world. Basically, on these ad networks, advertisers or brands can buy inventory themselves and run ad campaigns.

Secondly, there is the open internet, where publishers open up their ad inventory for real-time auctions where each impression is sold to the best bidder. Both price and the quality of the advertiser can be taken into account here, for example, Netflix will prefer to show an ad from Nike as opposed to one from OnlyFans. To run this auction process, key players are the supply side platforms (SSPs) and the demand side platforms (DSPs).

So, when a user visits a website or smartphone app, the publisher’s server will detect that an ad impression has become available. The server then sends a request to the publisher’s SSP which collects information about the consumer. Data collected can include age, gender, interests, browsing history, browsing behavior, intent, the smartphone device in use, typical engagement metrics and geolocation. The richer and more precise the dataset on the user, the more valuable the ad impression becomes.

The SSP forwards this impression to the DSPs, which evaluate the impression to place their bids. To more accurately value the impression, the DSP can join in additional data it has on the end user, which can have been collected by the DSP, the brand itself, or a third-party supplier. Data collection on internet users is a complicated industry as well, with tons of continuously evolving regulations.

Basically, The Trade Desk (TTD) is the dominant DSP as it has both the widest and best quality ad inventory available, some of the richest data sets on consumers, the best platform capabilities, and because it is an independent and neutral arbiter in the middle. This final point means that there is no conflict of interest between the advertiser and the DSP. Unlike Amazon’s or Google’s DSPs, TTD doesn’t own ad inventory itself, so it won’t try to unfairly promote its own impressions to advertisers. The sole aim of TTD is to identify the best available impressions for its customers.

Typically, advertisers make use of Amazon’s DSP when they want to run a campaign on amazon.com and similarly, Google’s DSP is mainly leveraged to run campaigns on Youtube. However, the aim of large brands is to re-target potential end customers across a variety of platforms and with different ads. So they might show you one ad on TikTok, another on Spotify, the Financial Times, X, LinkedIn, etc. To realize a multi-platform campaign like this, you basically need TTD.

An additional advantage is that a good DSP keeps track of which ad has already been shown to which end user. Showing a potential customer the same ad for the twentieth time is usually just wasted money. So a clever DSP can create substantial cost savings for customers as it can figure out when to change ads to re-target a customer or forego the impression altogether.

This is a former manager at TTD explaining the company’s strong position in the DSP market:

“The Trade Desk's value proposition is largely based on being independent as a neutral platform in the middle, while having access to large swaths of inventory across pretty much every streaming player within the connected TV (CTV) space, audio streaming, ads on mobile apps and every publisher within the programmatic space. Then, The Trade Desk has all sorts of connections to make it easy for the client to bring in their own and third-party data, while also additional data from a publisher itself can be integrated directly. For example, Disney might be willing to share some insights about their audience with The Trade Desk which can be tied to the available impressions.

In CTV, advertisers have been migrating their programmatic buying over to The Trade Desk. Historically, Roku was someone that you would have to work with directly and Netflix was in the same camp, but both are now opening up. And you can also buy Hulu inventory over The Trade Desk. There's a lot of opportunity in CTV.

Audio is another channel that is often forgotten, and players like Spotify and Pandora are integrated with the Trade Desk as well. Audio pales still in comparison with media spend on Connected Television, but it is growing because the audio platforms have authenticated and logged-in users, and having those types of identifiers is helpful in digital advertising.

The average client on The Trade Desk typically has an annual digital media budget upwards of $10 to $12 million, with some that are spending more than several hundred million a year. Probably more than half of these budgets on The Trade Desk are agency driven, both from major holdcos and smaller specialized agencies, but there are an increasing number of clients that are working with The Trade Desk directly. These have their own in-house teams of programmatic trading desks, but this is only for large companies because it's very costly.

The Trade Desk is now introducing AI to automate the setup of campaigns, effectively taking over that manual work that's placed on agencies or in-house trading teams. This creates an opportunity for smaller advertisers to work with The Trade Desk directly, as you don't have to rely anymore on sophisticated programmatic buyers to set up and manage your campaigns. You can now do this by pressing a few buttons and then smaller advertisers can also get into additional channels like connected television. Minimizing the burden of programmatic buying will allow more advertisers to move away from the ad networks of Google and Facebook—where you can activate a campaign with a couple of buttons and a credit card—to a platform like The Trade Desk.”

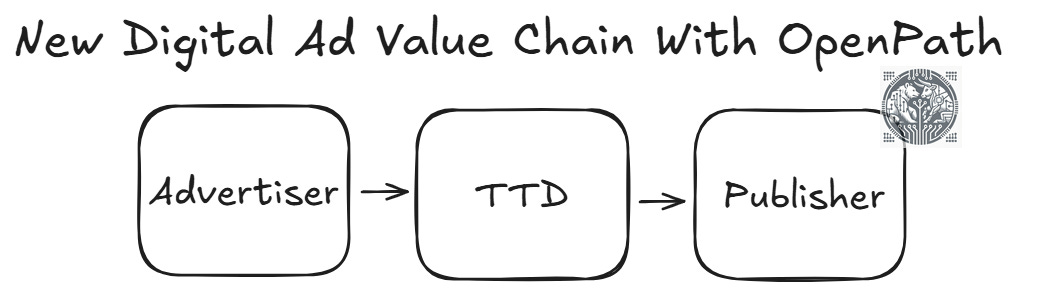

To further strengthen its strong position in the programmatic value chain, TTD has been building direct connections with the large publishers themselves. The attraction for publishers is that most brands are running campaigns on TTD anyways and so this way they can forego having to pay the SSP its take rate, which can be substantial. This new feature is what TTD calls OpenPath, and the attraction for TTD is that they can offer the widest and best quality inventory from the open internet on their platform. For example, one smaller agency mentioned in a Tegus interview that it was impossible for them to obtain ad impressions for the olympics on NBC, however, these easily became available to them via TTD.

So traditionally, we had the below value chain for digital ads on the open internet, i.e. an advertiser uses a DSP, to connect to a SSP and bid on an impression from a publisher:

However, with OpenPath, TTD is aiming to establish the below landscape, putting itself at the center to connect advertisers and publishers on the open internet:

The Trade Desk’s Future Growth Drivers

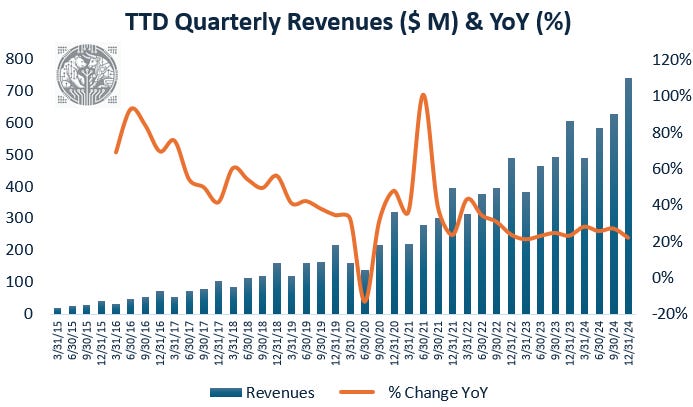

With the rise of the internet, TTD has been a spectacular growth story over the last decade. Quarterly revenues climbed from $18 million in 2015 to $741 million last quarter:

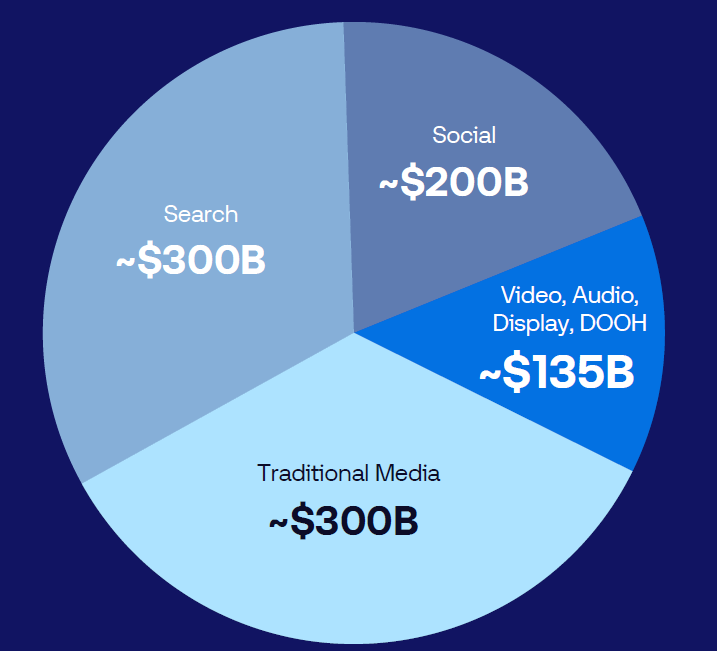

The company’s long term outlook remains strong. Obviously, OpenPath is a big opportunity for TTD to put itself at the center of programmatic advertising, and another large opportunity remains traditional media which is mainly comprised of linear TV these days. This is still a $300 billion global market, which continues to dwarf the small dark blue segment in the global ad market where TTD plays:

Basically, only $12 billion in annual ad spend is flowing through TTD currently while linear TV remains ripe for disruption, more on this in a bit.

To summarize the chart above, there are four blocks in the global ad market— search is dominated by Google, social is dominated by Meta, then there is traditional media which is mainly still linear TV, and finally there are the online video, audio and display (websites) markets, which are the bread-and-butter of TTD.

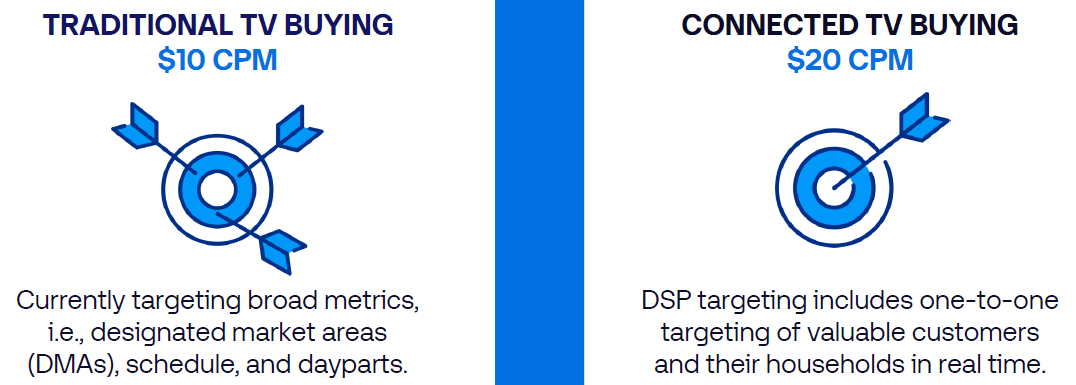

As the median age of linear TV viewers in the US is currently 65 years, this whole segment of the ad market will continue to move online in the coming decades. So traditional media will continue to shrink as eyeballs continue to move online. The other interesting feature of the online market is that ad pricing can be higher due to better targeting capabilities. TTD mentions that connected TV (CTV) typically sees a cost-per-mille (CPM, i.e. the price of 1,000 impressions) of $20 compared to only $10 for traditional TV:

The next bull argument is that TTD has a lot of runway for international expansion. Currently 88% of company revenues are coming from North-America, but the rest of the world actually contributes 60% of the global ad market:

Jeff Green, TTD’s founder, has regularly been discussing the company’s long term outlook during previous conference calls:

“A tailwind that is setting up The Trade Desk for continued outsized gains is the move to AI. Our AI product, Koa, is a great copilot for traders. But this is only the beginning, there are endless possibilities for us as we have one of the best data assets on the open internet. We're looking across our entire suite of products and are asking how they all can be advanced by AI.

Another factor that is changing the entire landscape of digital advertising are the changes happening at Google. Google has an incredibly dominant money-making business in search and another one in YouTube, with now also an incredible opportunity in cloud and AI. Because of these opportunities, Google could continue to downgrade their network business to focus on those prospects. After all, they operate at a disadvantage on the buy side of the open internet because Google lacks objectivity.

Google also has a pending antitrust trial that has created massive ripples throughout the global ad tech ecosystem. The outcome of the trial itself is less important than the change in behavior that will likely come from it, Google will remain under tremendous scrutiny from regulators around the world. The convoluted role they play in their network business, laid out very clearly by the US Department of Justice, is likely to result in more fair play. This presents a tremendous opportunity for us and for the broader ad tech ecosystem.

CTV is creating incremental secular tailwinds in the market. It's both our largest channel and our fastest growing. The premium open internet is where consumers are increasingly spending most of their time. Companies like Netflix, Roku, NBC, Spotify, Disney and Fox have redefined the consumers' internet experience over the last few years. You may remember at our last Investor Day, that we showed a graph of what our clients were willing to pay for CTV ad impressions on the open market and in many cases, we've been significantly higher than the price that the media companies were negotiating themselves in direct deals.

The content arms race is more intense than ever and media companies need to monetize their content as effectively as possible. Two weeks ago, Variety reported that the top six media companies will increase content spending this year by 9% to a record $126 billion, all of which needs to be funded. Media companies now need to provide advertisers with more insights and tools like UID2 and OpenPath are helping provide that signal.

Many of the major CTV players around the world are aggressively implementing OpenPath now. One major news publisher saw their revenue increase by more than 25% with OpenPath. Disney is now working towards 75% of their ad sales being automated by 2027, with the vast majority of those impressions being biddable. Another CTV leader that has embraced OpenPath is VIZIO, which has more than 24 million active devices in the United States and more than 300 ad-supported CTV channels. VIZIO deployed OpenPath and saw a 39% improvement in revenue from our platform. Because of the number of deals that we've signed recently, we are extremely confident that 2025 will be the year when OpenPath enters the steep acceleration phase of its S-curve growth.

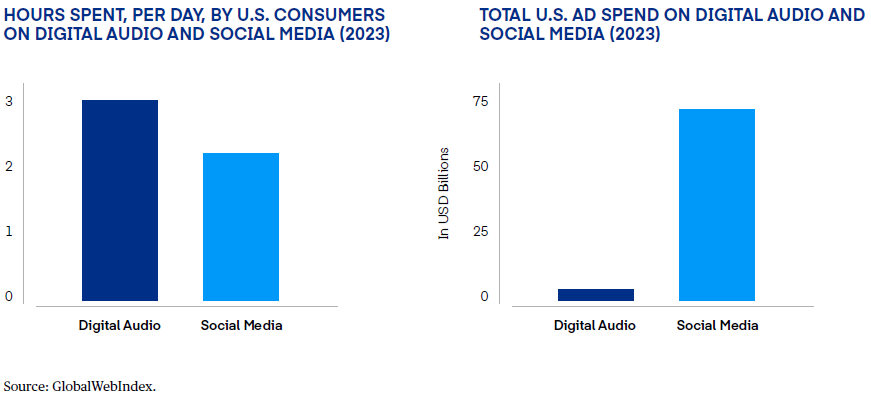

A next growth vector for us is audio. The biggest players in audio are global and they can capture one of the biggest opportunities in advertising and media today, which is the delta between time spent in the audio channel and the amount of ad budgets heading to that channel. Digital audio is at the early stages of its evolution and the channel is in a similar position to where CTV was a few years ago. Consumers in the US spend an average of 3 hours per day consuming digital audio, up significantly over the last 5 years, and advertisers are eager to capitalize on this emerging advertising channel. Spotify has been at the forefront of this mass consumer shift and is building out their programmatic capabilities.

Then we have a massive opportunity in retail media. Amazon has showcased the benefits of using purchase data to make retail businesses work better. And finally, we have live sports. Sports is some of the most premium content and media, it is scarce and highly sought out by brands, and it is built for programmatic advertising.”

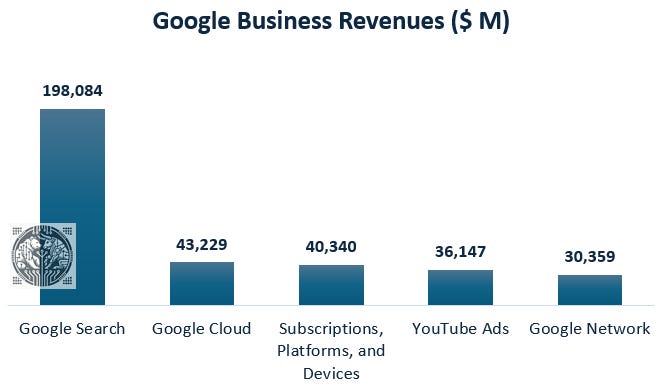

The opening up of Google’s network business is a large opportunity. In this business segment, independent apps and websites can leverage Google’s adtech technology to show ads to their users. So this is a separate business from search and Youtube, and includes adtech such as AdSense, AdMob and Google Ad Manager. As in all of its markets, Google is very dominant in this space and this has been drawing attention from regulators around the world.

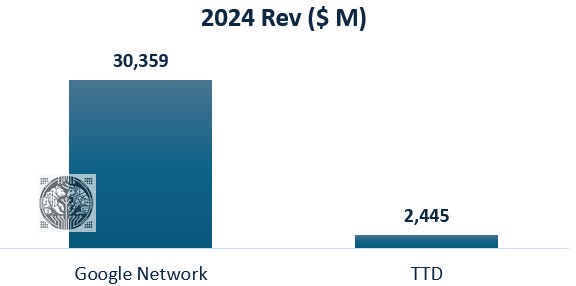

If Google would have to open up its network business by making these impressions on third-party apps and websites biddable, it represents a big opportunity for TTD. Google Network alone, i.e. Google’s smallest business unit, is more than 12x the size of TTD:

As mentioned, Google Network is the company’s smallest business unit:

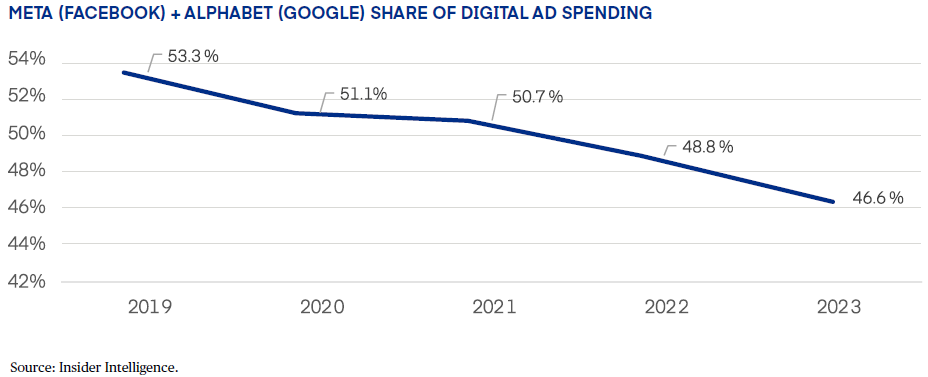

An organic growth story for TTD is that there are a wider variety of popular apps today that audiences are spending large amounts of time in. Ten years ago, these types of dominant apps were mostly Facebook, Instagram and Youtube; but now you have as well TikTok and Netflix being major apps, and with also a number of other large platforms that continue to gain scale such as Spotify, X, Reddit, Hulu, Roku, LinkedIn, Amazon Prime, Pinterest, etc. The good news is that most of this inventory is accessible over TTD, allowing the leading DSP to gain share in the overall ads market. As a result, the share of the two dominant walled gardens in the digital ads world—Meta and Google—has been falling:

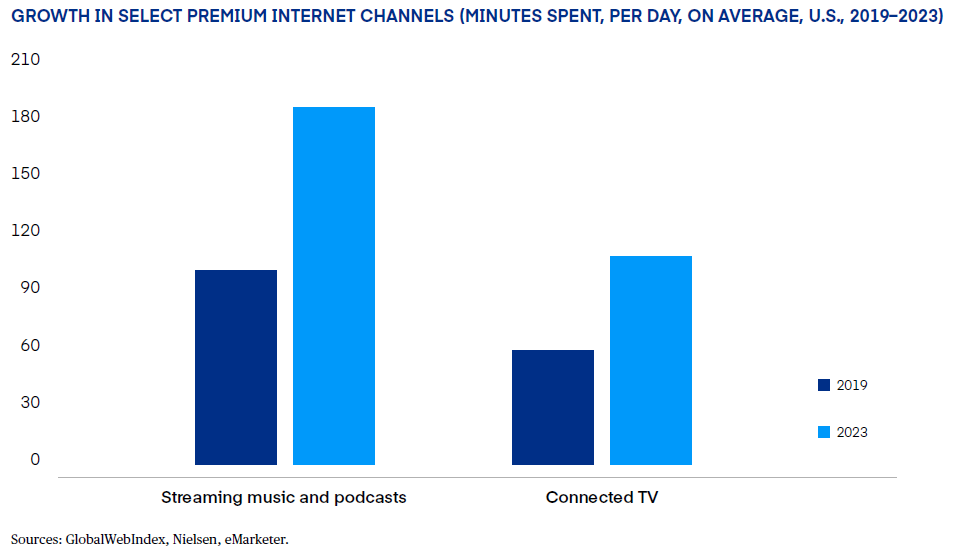

Audiences are spending especially more time in audio and connected TV apps:

Although both of these are largely monetized via subscription models currently. However, as 63% of Spotify’s active users are currently ad-supported, there is a large opportunity to increase revenues from this user base by integrating them into OpenPath. Similarly, for Netflix, a new ad-based revenue model is one of the key growth stories for the coming years. A compelling advantage with both the audio and CTV formats is that you can’t skip the ad, whereas on social media such as Facebook, many just quickly scroll past the ad while largely ignoring the content.

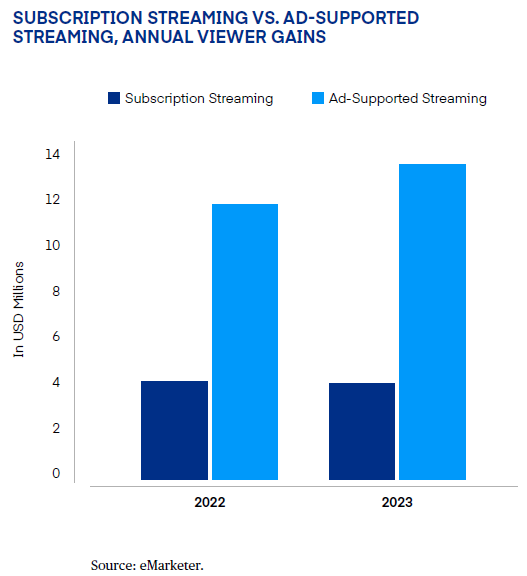

Also in CTV, most of the audience growth is in ad supported streaming:

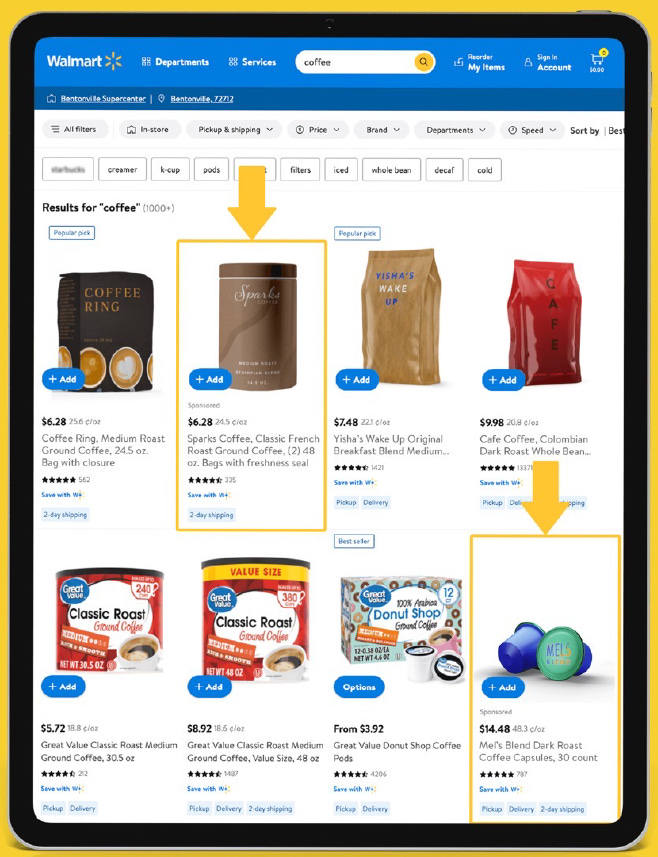

Finally, retail media networks are a great way for brands to promote their products. For example, if you’ve launched a new coffee brand and want to boost sales on walmart.com, you can bid for prime ad inventory. Many e-commerce sites are now realizing this so this should remain an attractive opportunity.

Thus, all was looking really good for TTD and this was a consensus long for many active equity managers. However, the combination of a valuation that required perfect execution, the recent earnings miss, and the subsequent overall market sell-off due to macro fears caused the company’s share price to fall off a cliff:

The Q4 Miss

This is Jeff Green again, discussing what went wrong in the quarter:

“For the first time in 33 quarters as a public company, we fell short of our own expectations. For Q4, the reality is that we stumbled due to a series of small execution missteps while simultaneously preparing for the future. That said, we see a larger and faster-growing market than we originally expected, and this is why we are recalibrating our larger company for an even stronger future. I want to highlight four major changes we've made at The Trade Desk in the last few months.

First, we did the largest reorganization in company history in December. For most people in the company, we provided a much clearer view of their roles and responsibilities, and that mostly also meant a change in reporting structure. Additionally, we streamlined client-facing teams to reduce complexity. Now, some teams will focus on brands while others will focus on agencies. Our commitment to agencies remains strong, but we are also expanding brand direct relationships, particularly through joint business plans (JBPs) which grow 50% faster than the rest of our business.

Second, we understand that this moment requires us to scale our internal operations and we will hire senior talent to support long-term growth. For example, we've done all of this without a COO for some time and there is absolutely no reason why we shouldn't add a world-class COO to the team. There are opportunities for us to get more efficient internally and operationally more rigorous.

Third, we have increased our resource allocation on brands. Advertisers are becoming more strategic and data-driven in their media buying decisions and that's great for us. While this shift has caused short-term fluctuations, it's ultimately aligned with our long-term strength. This is evident in the growing number of JBPs that we've secured with over 100 of the world's leading brands, and many of them in the second half of last year.

Fourth, we revamped our product development process, shifting back to smaller and more agile development teams that release updates weekly instead of drifting towards waterfall methods. Our engineering team is now divided into nearly 100 scrum teams to more easily ship and collaborate with the business teams. I expect this to accelerate Kokai enhancements and to complete the transition of 100% of our clients from Solimar to Kokai during this calendar year.

During the quarter, there were a series of decisions we could have made to enhance the short-term performance of the company and neglect the long-term. We consistently chose to focus on the long-term opportunity as this is in the best interests of all our stakeholders.”

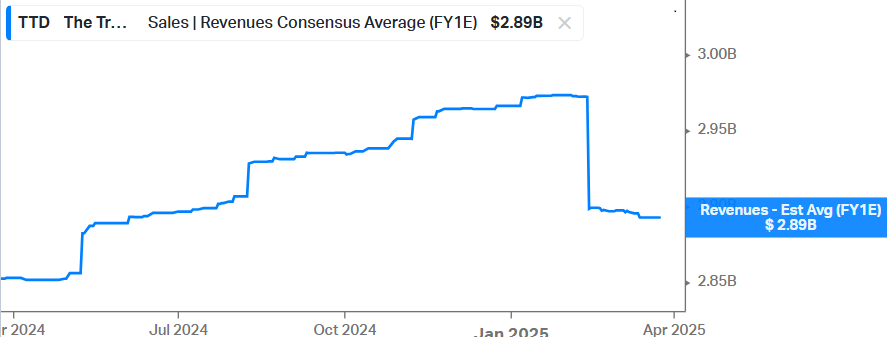

We already saw above in TTD’s revenue growth chart that growth remains robust. However, due to the miss and the weaker than expected Q1 guidance, the market is now looking for 18% top line growth in 2025. You can see below that estimated revenues for the year basically got downgraded from $2.97 billion to $2.89 billion, i.e. a downgrade of 2.7%:

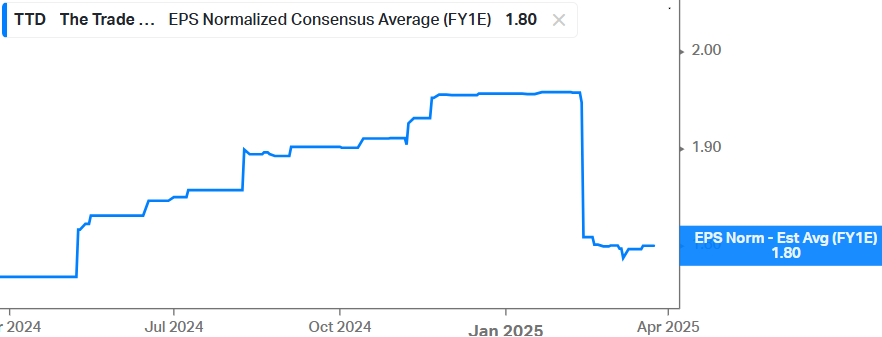

While EPS were downgraded by 8.6% due to operating leverage:

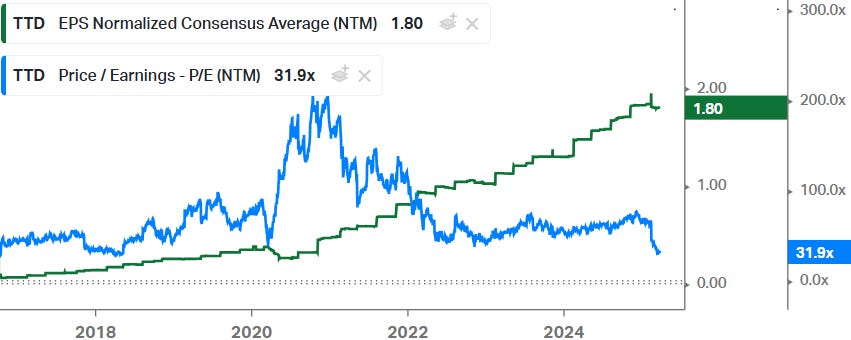

Thus, most of the 52% share price fall has been due to multiple compression, with the shares now trading at their cheapest valuation since IPO:

For premium subscribers, we’ll dive into current developments in the adtech industry and we’ll share the insights from a VP at one of the world’s largest ad agencies, with over $16 billion in annual revenues, on both current developments in the industry and for TTD. Additionally, we’ll review the various bear cases that caused the shares to sell off sharply such as rising competition, concerns about take rates and whether TTD’s new platform rollout—Kokai—has been botched. Finally, we’ll review the financials and valuations of key stocks in this space and which ones we see as top picks here, and whether TTD should represent a buying opportunity or whether this is a falling knife.