An Emerging Monopolist

A deep dive

Introduction

Companies that dominate their industries are often amongst the best performing assets. These types of companies usually have strong pricing power, which translates into high EPS growth due to high incremental margins. Subsequently, earnings can be used to buy back shares, which again fuels EPS growth. So it’s not uncommon to see these types of stocks compound over multiple decades, translating into outsized returns for shareholders.

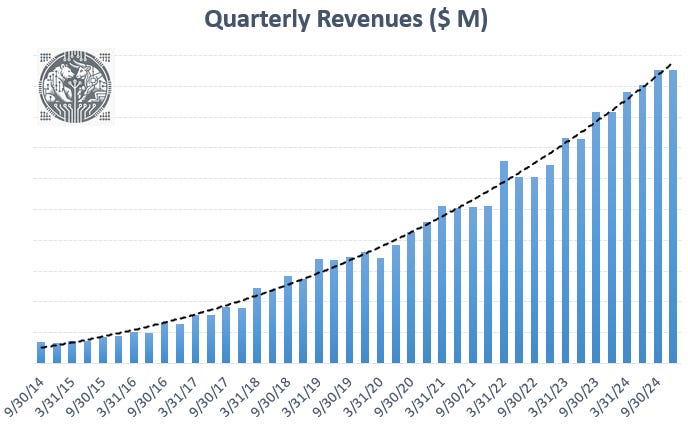

Today, we will do a deep dive on a name that is on its way to consolidate its global industry. Barriers to entry are high, as the company managed to build its compelling platform by decades of investment. Currently, there isn’t a single competitor which can offer a suitable alternative. While valuation isn’t cheap, the stock has gotten a lot cheaper following the market sell off in the last few weeks, and the company is very profitable while continuing to drive high double-digit top line growth rates. Additionally, EPS growth is at 1.5x those top line growth rates as incremental margins are very high. Finally, there is very limited share-based compensation so investors are getting a clean earnings number.

The company definitely isn’t a household name, in fact, we’ve never seen it mentioned on social media such as X. Although investors reading a variety of business newspapers will have seen the occasional article on the company. It’s a mid-cap that has sufficient liquidity even for large funds to take a position. We see an IRR of 21% in this name in the coming years and with plenty of potential to exceed that due to the company’s new products, which have strong potential to surprise the market on the upside. This should be an interesting name both for shorter term investors, as well as for Warren Buffett-style long term investors who are happy to hold companies for 5-10 years.